KEY

POINTS

- Private credit generates higher yields because capital is locked up for years.

- Institutional investors can tolerate illiquidity; most retail investors cannot.

- Retail private-credit funds introduce valuation opacity and withdrawal restrictions.

- Management fees of 1-2% significantly reduce investor returns over time.

- If retail investors pull back, private lenders may tighten credit and raise borrowing costs for mid-market companies.

BlackRock’s ambitious push to bring private-credit investing to the masses is running into a sobering reality: retail investors don’t want it—or at least, not on these terms.

The $12 billion acquisition of HPS Investment Partners was supposed to be BlackRock’s golden ticket into the explosive world of private credit. The pitch was simple: give everyday investors access to the same high-yielding debt investments that have enriched institutional players for years. Democratize private credit. Unlock returns. Build a new revenue engine.

Instead, the market is sending a different message: be careful what you’re selling to people who don’t understand the risks.

The Setup

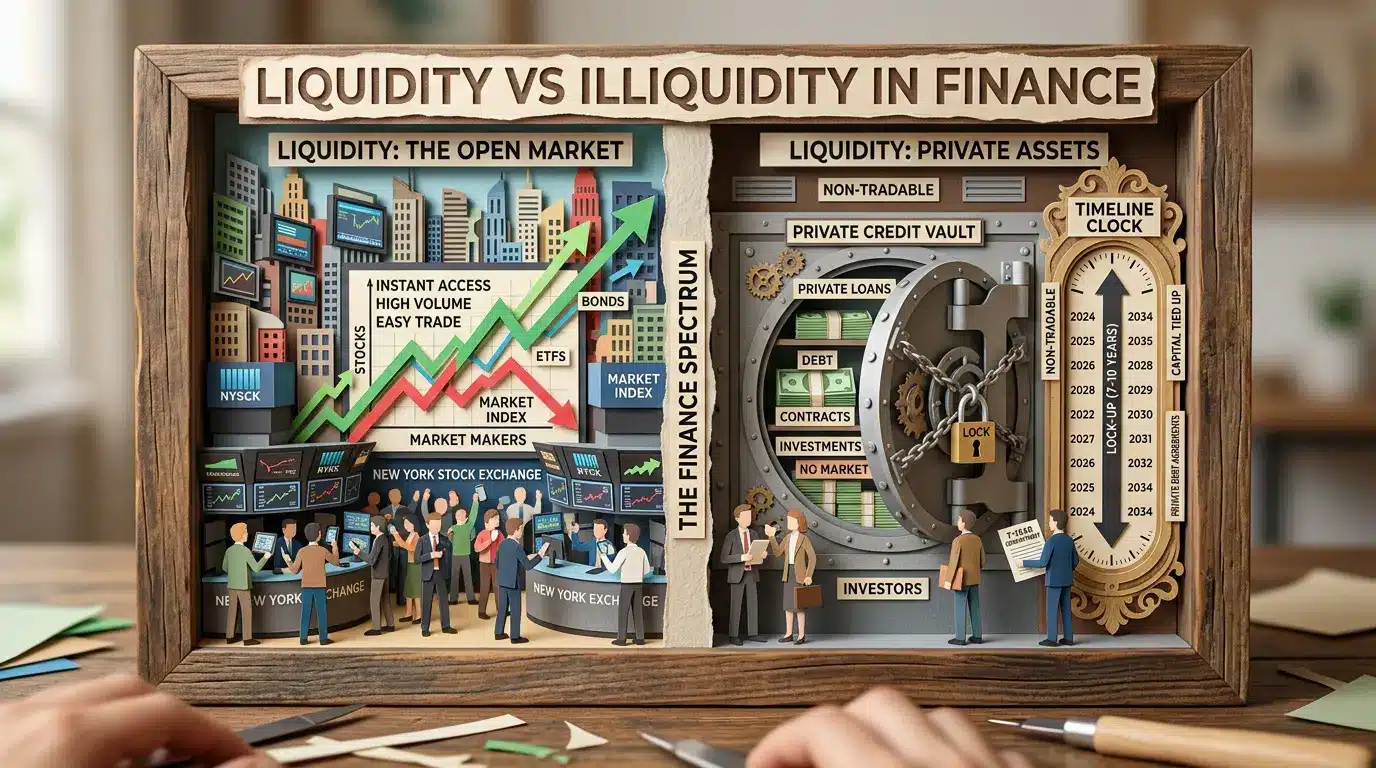

Private credit has been one of the hottest asset classes over the past five years. While public bonds yielded meager returns, private lenders—the firms that lend directly to mid-market companies outside the traditional banking system—were charging 10%, 12%, sometimes 15% on their capital. The returns looked magical compared to public markets.

BlackRock saw the opportunity. By acquiring HPS, they gained control of one of the largest private-credit platforms in the world, with tens of billions in assets under management. The plan: bundle these illiquid private loans into products retail investors could buy through their brokerage accounts. Take a cut of the management fees. Sit back and watch the recurring revenue flow in.

On paper, it made perfect business sense.

The Problem: Illiquidity Meets Retail Reality

Here’s where it gets complicated. Private credit works because the loans are illiquid. The lender commits capital for years and earns a premium for that illiquidity. Institutional investors—pension funds, endowments, insurance companies—can afford to lock money away for 5-10 years. They have diversified portfolios. They understand the risks.

Retail investors don’t have that luxury.

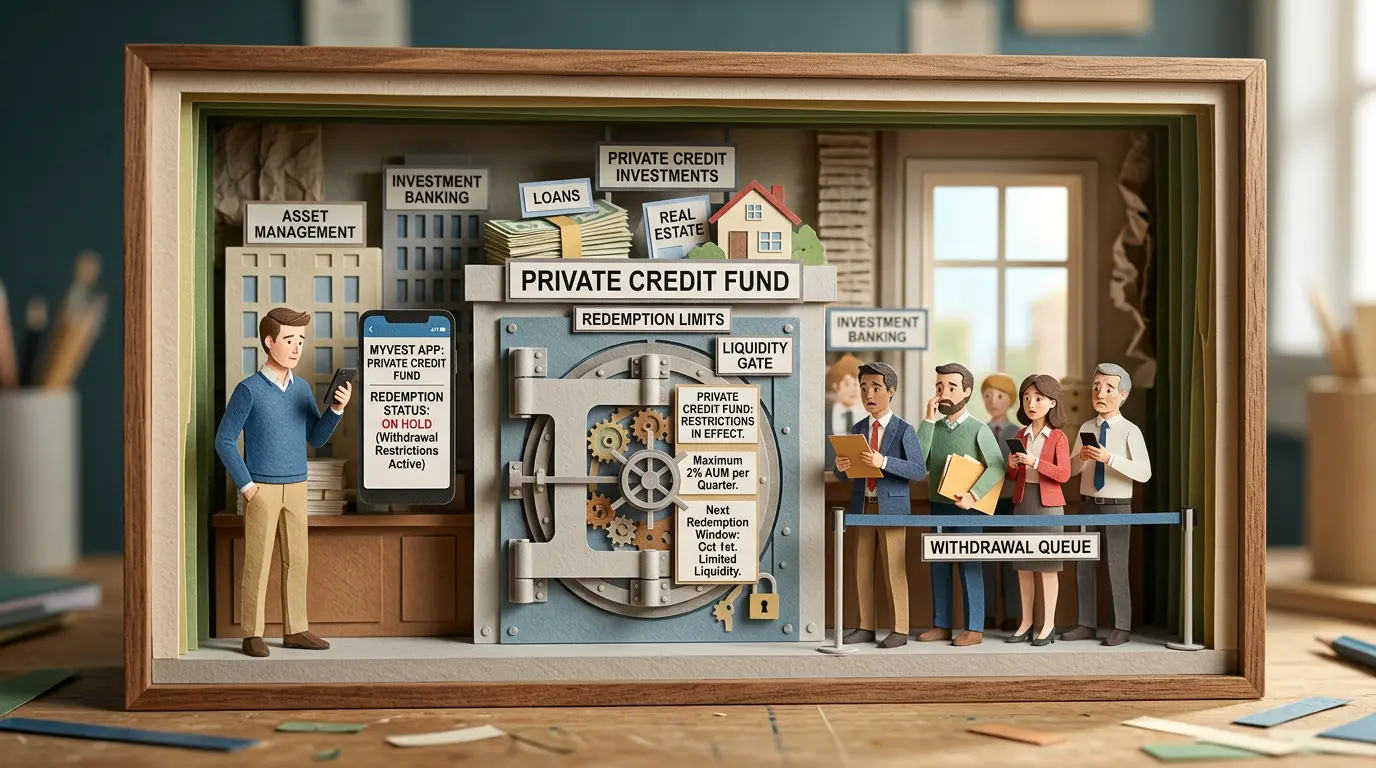

When a retail investor buys a stock, they can sell it tomorrow. When they buy a bond, they can trade it on a secondary market if they need cash. But when they buy a private-credit fund? They’re committing capital to loans they can’t easily exit. The fund manager decides when you get liquidity—if at all.

And recently, some of BlackRock’s private-credit funds started limiting withdrawals. Investors wanted their money back. The fund said no, not yet. That kind of friction destroys trust fast.

The Valuation Opacity Problem

Here’s another issue. With a stock, you know what it’s worth every second of the trading day. With private credit, you don’t. The fund manager marks the loans at subjective valuations based on their assessment of the borrower’s health. If you want to know how much your investment is worth, you’re taking the fund manager’s word for it.

This works fine when you’re a pension fund with a 30-year horizon and a sophisticated risk management team. But for a retail investor checking their Robinhood or Fidelity account every month, it creates anxiety. You see a number. You don’t know if it’s real.

When things are booming and valuations are rising, nobody complains. But when the credit cycle turns—when those mid-market companies hit rough patches and loan defaults start ticking up—valuations reset lower. And you’re stuck holding the bag.

The Fee Drag

Private-credit funds charge management fees of 1-2% annually, sometimes more. That’s not unusual for institutional investors, but retail investors are conditioned to paying near-zero for index funds. A 1-2% annual drag compounds fast over time. If the fund generates 8% returns gross, you’re netting 6-7% after fees. That’s still decent, but it’s not the 10-12% yield that marketing materials dangle in your face.

The Skepticism

Wall Street is watching this play out and asking hard questions. Can retail investors really commit capital for 5-10 years without needing liquidity? Do they understand what happens when the valuation marks reset downward? Are they prepared for the illiquidity?

Rating agencies like Moody’s have already warned that retail investors are not prepared for this level of complexity and illiquidity. And the market is starting to agree.

BlackRock’s broader private-markets expansion—not just private credit, but private equity, private real estate, all bundled into products for retail—is facing headwinds. Investors are pulling back. The mystique is wearing off.

Why This Matters to Business Owners

If you’re a mid-market company owner or CFO, this matters to you in two ways:

First, these private-credit funds are your lenders. If retail investors start pulling back and demanding liquidity, these funds might tighten lending standards or charge higher rates to compensate. That could make growth capital more expensive for companies like yours.

Second, this is a window into what not to do. If you’re selling products or services to customers, selling complexity wrapped in simplicity is a dangerous game. BlackRock thought they could take institutional-grade private credit and retail-wrap it. The market is saying: not without massive skepticism and friction.

The Bottom Line

BlackRock’s $12 billion HPS acquisition is a solid business strategically. But the retail private-credit push is hitting reality. The returns are real, but the complexity and illiquidity are real too. You can’t democratize something that fundamentally depends on lock-in periods and illiquidity without creating friction.

For retail investors tempted by private-credit yields: the extra 2-3% over public bonds isn’t worth the illiquidity, valuation opacity, and fee drag unless you genuinely don’t need the money for a decade.

For BlackRock, the lesson is humbling. You can’t solve the retail-institutional mismatch with a slick mobile app and a low minimum. Some products are built for institutions. Trying to force them to retail is a long-term value destroyer.

The market is calling it out. And that skepticism is probably justified.